Japanese government bond yields have been on the rise, with 10-year issues hitting 2.35% on 20 January. There are numerous causes driving the sell-off in JGBs.

- The Bank of Japan has increased its overnight interest rate from -0.1% in early 2024 to 0.75% and futures markets suggest it will rise to 1.2% by the end of 2026. Some economic forecasts suggest interest rates could even go up to 2.0%.

- There are concerns over government debt levels and the potential for renewed fiscal stimulus after 8 February’s snap general election. Should Prime Minister Sanae Takaichi strengthen her mandate, tax cuts and higher defence spending are expected to follow.

- The economy has been growing quickly, with nominal GDP growth close to 4.5% in 2025. There are concerns over structurally lower demand for long-term JGBs. The market is likely to remain sensitive to policy developments.

However, 2026 should see lower inflation (the consensus forecast calls for around 2.0%). This could help stabilise yields. In the meantime, potential repatriation flows into the yen market might contribute to higher global bond yields and currency volatility.

In short, Japanese yields are in a new medium-term equilibrium range between 2% and 3%.

Equities weather geopolitical storm

The dollar and gold price might tell a different story, but equity markets have shrugged off the geopolitical turmoil seen over the last month. This is partly because the impact on economic growth and corporate profits of events in Venezuela and Greenland is less clear than it was for last April’s ‘Liberation Day’ tariff announcements.

In addition, recent economic data has generally been better than expected. The key determinant for the direction of equity markets in the near term will be the current earnings reporting season.

At the time of writing, around 143 companies had reported. The figures have been encouraging: aggregate earnings growth of 11% and absolute earnings more than 10% above expectations, according to FactSet.

Last year’s outperformance by the technology sector, however, has not been repeated so far this year, or at least not entirely: the tech-heavy Nasdaq 100 index has just barely outperformed the MSCI Europe after initially lagging.

In emerging markets, though, artificial intelligence remains the key driver, with technology stocks in the region advancing by nearly 12% so far this year. We expect that pace of appreciation to slow, while US tech stock gains pick up speed.

Fed succession: This time is different

After January’s gathering of the rate-setting Federal Open Market Committee, Jerome Powell, Chair of the US Federal Reserve, will lead only two more meetings – one in March and one in April – before his terms ends in May.

President Donald Trump has nominated Kevin Warsh as his replacement. The succession at the head of the Fed has always attracted the attention of economists, but this time is different. Statements on monetary policy by the president and Treasury Secretary Scott Bessent have raised concerns among investors over the Fed’s independence being impeded.

Why does this matter? Many central banks are accountable for their actions to the respective Parliament (or Congress, in the case of the US). Is this preferable to answering to politicians? The answer is ‘yes’.

A recent ECB study of 155 central banks over 50 years concluded that “independent central banks are able to pursue more credible monetary policies and are therefore more effective at keeping inflation under control.”1 In other words, independence allows central banks to move away from short-term (political) objectives and focus on their core mandate.

A loss of credibility could de-anchor the inflation expectations of businesses, investors and consumers. That could result in a rise in long-term bond yields, which could harm financial markets (including equities) and the broader economy.

Monetary policy is not only about setting interest rates.

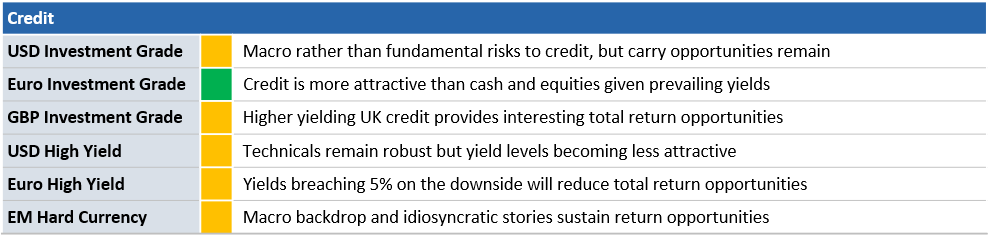

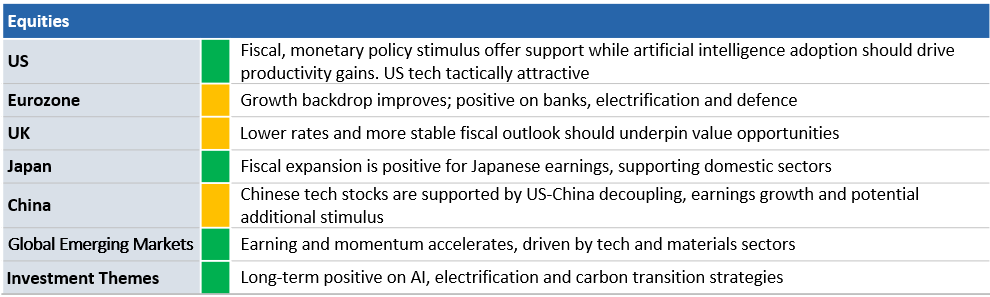

Asset class views

[1] Why central bank independence matters – lessons from the past 50 years