After a decade dominated by the strength of US equities, European stocks have been staging a notable comeback in 2025. With attractive valuations, favourable monetary policy at the European Central Bank, and structural tailwinds driven by unprecedented fiscal stimulus, Europe offers meaningful potential for investors.

Attractive valuations relative to the US

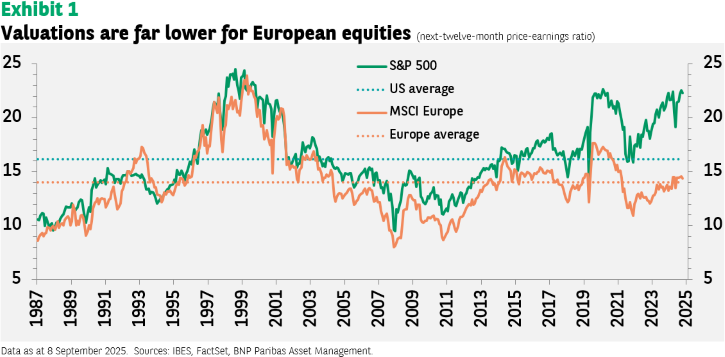

We believe attractive valuations are a powerful argument in favour or European equities: they currently trade at significant valuation discounts compared to US stocks.

The next-twelve-month price-earnings ratio for the MSCI Europe index is currently 14.6x. That is slightly above the average since 1987 of 14x. By contrast, in the US, valuations are close to all-time highs, currently at 22 times expected earnings. Furthermore, Europe’s average dividend yield of near 3.3% substantially exceeds the US average of about 1.3%.

Europe’s recovery in earnings looks bright

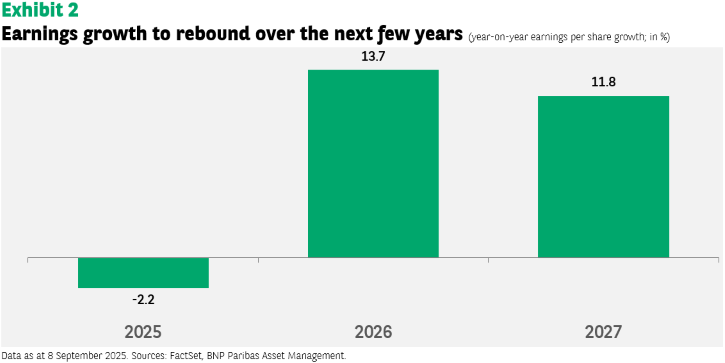

We believe the outlook for European company earnings is brighter than it has been in many years. Consensus estimates for profit gains over the next couple of years see a substantial improvement in results compared to 2025, as Exhibit 2 shows.

The expected gains are particularly high in industries such as biotechnology (34% estimated earnings per share growth in 2027 over 2026), semiconductors (24%), and aerospace and defence (17%).

Unprecedented increase in defence and infrastructure spending

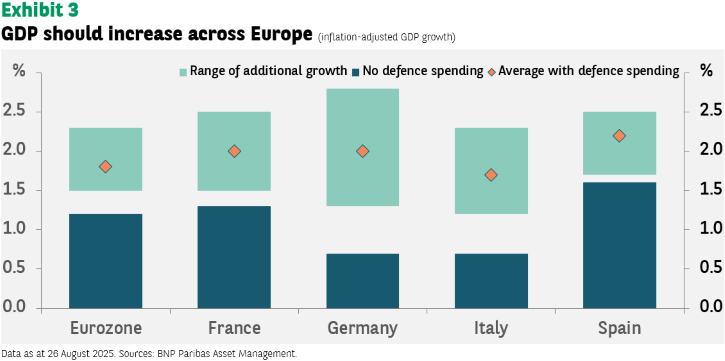

US President Donald Trump’s push for greater defence burden sharing by Europe has borne fruit. There is broad acceptance now across NATO countries to spend 5% of GDP on defence (broadly defined). We estimate the increase in defence spending could double the rate of real (inflation-adjusted) GDP growth across the European region.

In addition, Germany has launched a 12-year, €500 billion infrastructure and defence investment initiative including infrastructure, construction, renewable energy, healthcare and defence.

This is a huge change for Germany and Europe, which has historically been reluctant to spend on such a scale to boost growth. These outlays should have a meaningful impact on the continent’s growth rate as there is significant spare capacity in its economy.

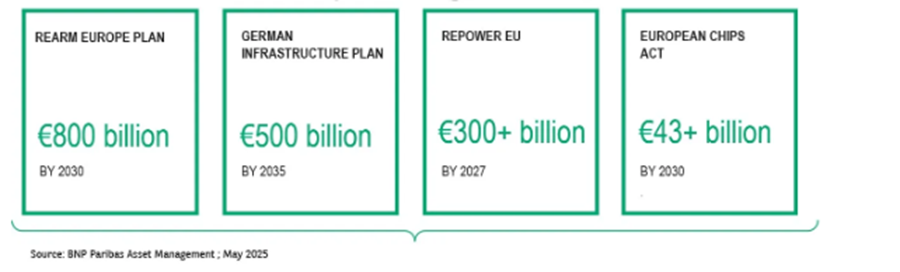

Europe’s pursuit of strategic autonomy has emerged as a central priority. For the region to act independently in key areas such as defence, energy, digital infrastructure and critical supply chains, investment plans for public initiatives of a historic scale are in the pipeline. These reflect the fundamental changes in the geo-political environment.

Planned investments in Europe’s strategic autonomy amount to over €1.6 trillion

European fixed income also offers opportunities

A crucial argument in favour of European fixed income is the market’s confidence in the ECB to remain vigilant about inflation risk. Bondholders can rely on the central bank to protect them from inflationary pressures.

European bonds, and in particular corporate debt, have continued to do well with relatively low volatility. In the first half of 2025, this market has again shown resilience in the face of considerable uncertainty.

European growth has been robust in the first half and there is scope for a further pick-up in corporate investment and mergers and acquisitions as the economy gains momentum over the next 12 months. Corporate debt issuers have continued to prioritise deleveraging.

Inflows into mutual funds and demand for collateral for collateralised loan obligations (CLOs) are bolstering demand.

Our analysis shows the fundamental characteristics of companies in the euro high-yield segment are relatively solid. Corporate results have continued to demonstrate the resilience of business models. Profit margins have been stable, costs are well under control and there is potential for cash generation and balance sheet improvement.

While we see limited scope for further significant spread tightening in 2025, we expect carry and security selection to drive performance.

Capital meets opportunity for private assets

In addition, private capital is positioned to help reshape the European continent’s competitiveness by driving innovation, creating regional champions, and mobilising the sizeable investments required. We believe Europe is emerging as one of the most compelling destinations for private asset investments.

The case for Europe factors in a gap in market valuation between European companies and their US-listed peers and falling financing costs. But it is primarily based on a growing conviction that economic reforms, combined with a stable environment for long-term investments, are paving the way for major opportunities across Europe for all investors.

Europe offers macroeconomic and policy stability — combined with a highly investable structural roadmap. Public plans are creating tangible project pipelines and co-investment frameworks — not just wish-lists. Private capital is explicitly sought after to complement and scale up public capital across asset classes. Deployment is aligned with long-term objectives: impact, resilience, energy security, and re-industrialisation.