Euro high-yield bonds have continued to perform well with relatively low volatility, showing resilience in the face of considerable uncertainty. Olivier Monnoyeur sees even brighter prospects ahead and reports on our positioning in sectors where the trough is either near or behind us.

There are fewer tailwinds for eurozone high yield from falling interest rates this year. The asset class saw robust performance over the last two years (benchmark returns of 12.4% in 2023 and 9.2% in 20241). Performance this year through the end of July was 3.7%, on course to return 6% for the full year. That is close to the carry offered by the asset class.

We see the current environment as supportive for eurozone high yield. The eurozone economy grew by a cumulative 0.7% in the first half of 2025, slightly above the 1.2% annual trend rate of growth. We expect the economy to regain momentum going into year-end.

The crippling uncertainty over tariffs appears largely over for now. The trade deal between the US and the EU — with a 15% tariff on most goods imported from the EU — is painful, but better than the 30% tariff US President Donald Trump had previously proposed. At the very least, the deal gives European businesses clarity on the operating environment.

European companies have coped well with uncertainty

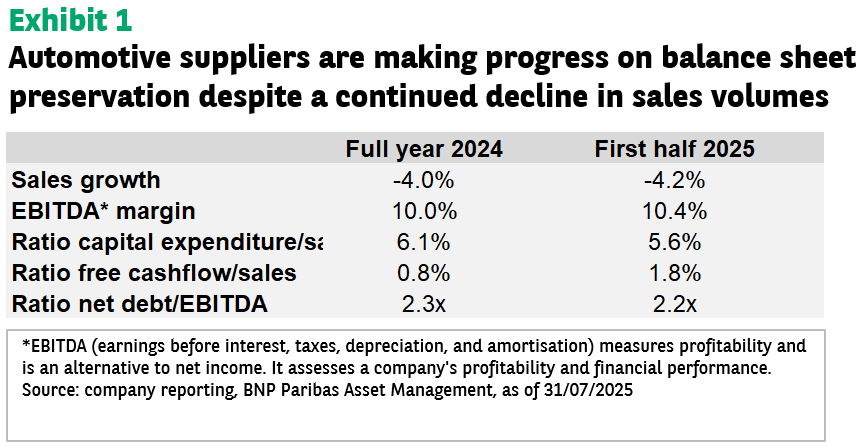

We see better prospects for several sectors in the European high-yield segment. The car industry (which makes up 11% of our index), is a prime example of a sector burdened by negative sentiment.

We increased our allocation to cars from close to zero at the start of the year to around 7% on the view that the decline in sales has not been as bad as initially expected and that balance sheet protection measures are starting to bear fruit (see Exhibit 1). We initiated allocations to both manufacturers and suppliers with a preference for the latter.

The structural crisis the industry faces was well documented even before the imposition of tariffs. European manufacturers face competition from China, a challenging transition to electric vehicles, and a high-cost structure with low-capacity utilisation pressuring margins.

As a result, the sector has been in a cost-cutting cycle for the past two years, closing plants and increasing the efficiency of capital expenditure. The benefits of these measures were apparent in second-quarter earnings reports, which saw suppliers to the industry do better than manufacturers. These themes have played out well for us over the last two months.

Increasing allocations to under-owned sectors

We began the year somewhat defensively in terms of sector choices. We were overweight less cyclical sectors such as healthcare and real estate, which are not as exposed to tariff risk.

In July, we increased our allocations to cyclicals and lagging cyclicals such as chemicals. As was the case with cars, sentiment was negative towards the sector.

We believed the negative sentiment was excessive. While we did not believe a trough in performance was necessarily imminent, we took positions in those names that our analysis suggested were sufficiently robust to weather the storm for a few more quarters.

Looking through the trough for high-yield debt

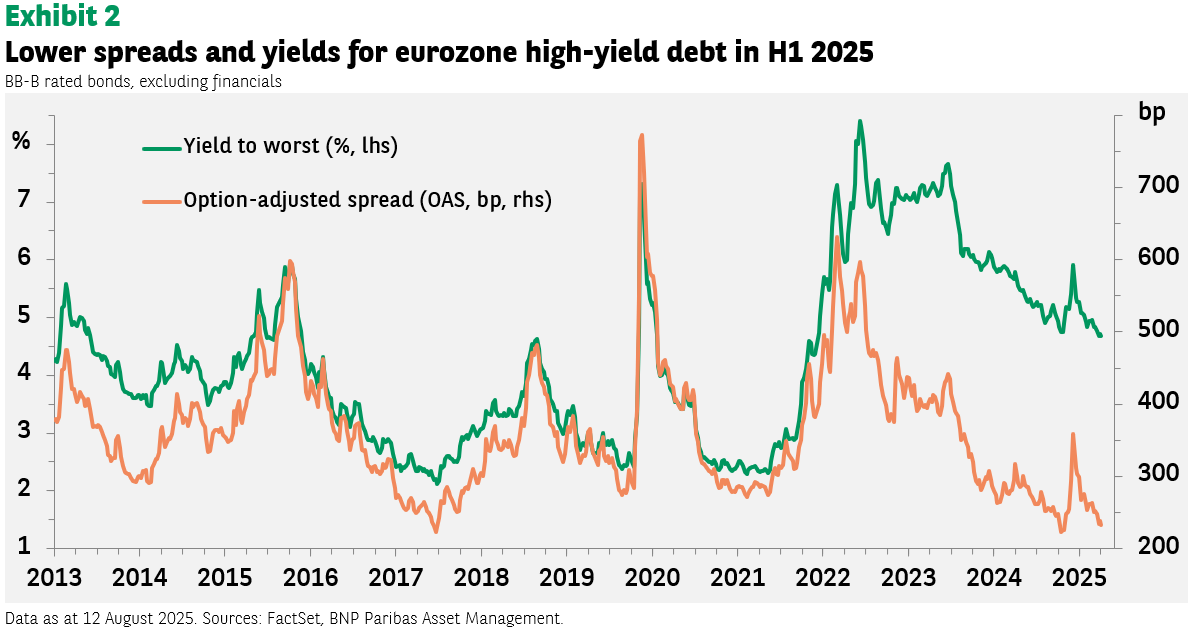

The second-quarter corporate reporting season has been reassuring, with solid earnings even in sectors under pressure. With the tariff issue hopefully now behind us, we are constructive on the outlook and favour carry. The spread of the index, however, is tight at around 230 basis points (see Exhibit 2).

There may be limited scope for further spread tightening, but by selecting corporate bonds that our analysis suggests will survive in some of the poor performing, neglected sectors, we believe we can build a portfolio that outyields the index. Once through the trough, these are bonds that should be in demand, potentially generating excess return.

Despite the tight credit spreads, there is currently a more pronounced dispersion in spreads (that is, the percentage of bonds trading at least 100bp tighter or wider than the average index spread) than in similar periods previously.

As a result, there is a broad range of investments from which we can select bonds offering good potential returns. We employ in-depth credit research to identify opportunities at the issuer, sector and regional level.

A tailwind – Fiscal push in Germany

We have been seeking to identify those companies that stand to benefit from increased government spending on infrastructure and defence. German industry has struggled over the past two years, but we believe now is the time to position for an improvement in 2026.

Construction is one sector where we see potential. The sector has been under pressure for more than two years, and in countries such as France, construction is still deep in contraction. But we are starting to see green shoots and scope for stabilisation later in the year and a possible acceleration in 2026.

Activity in the primary market reflects increased risk appetite

The primary bond market was active in the early summer. In June, we participated in around 15 new deals compared to 2-5 during a ‘normal’ month. This strong new issuance activity reflects an improvement in risk appetite with inflows to the asset class. There are signs that animal spirits are returning. That may translate into increased merger and acquisition (M&A) activity, which could benefit high-yield companies.

This could involve companies that need to sell non-core activities to accelerate reaching their debt reduction targets. This trend has already picked up in 2025 and we think the environment remains favourable for it to continue.

We can benefit from it by identifying companies that can pay down their debt faster than expected via the proceeds of asset sales or as a result of being purchased by competitors or private equity companies.

What is next for euro high-yield bonds?

European economic growth has been resilient in the first half of 2025. There is scope for a further pickup in corporate investment and M&A as the economy gains momentum over the next 12 months.

Companies in the high-yield credit segment continue to prioritise debt reduction. Inflows into mutual funds and appetite for collateral for collateralised loan obligations (CLOs) continues to bolster demand for these corporate bonds.

Our analysis shows the fundamental characteristics of companies in the euro high-yield segment as relatively solid. Company results are demonstrating the resilience of business models. Profit margins are stable, costs are well under control, and there is potential for cash generation and balance sheet improvement.

While there is limited scope for further significant spread tightening in 2025, we expect carry and agile security selection to drive the performance of our strategy.

[1] The ICE BofA ML BB-B European Currency Non-Financial High Yield Constrained index contains all non-financial securities in the ICE BofA ML European Currency High Yield Index rated BB1 through B3, based on an average of Moody’s, S&P and Fitch, but caps issuer exposure at 3%.